Swing High Low by MIRRORPIPThis strategy finds swing high and lows and marks them as SH and SL respectively.

if the pattern tries to form higher high it will trigger a buy signal

if the pattern tries to form lower low, it will trigger a short signal

This setup is very popular among price action lovers

Cerca negli script per "high low"

Multi Channel GRID & DCA LTF [trade_lexx]Multi Channel GRID & DCA LTF

Usage Guide

Part 1: The concept and general possibilities of the "Multi Channel GRID & DCA LTF" strategy

Introduction

Welcome to the guide to "Multi Channel GRID & DCA LTF", a powerful and versatile automated trading strategy for the TradingView platform. This tool was developed for traders who are looking for flexibility, control and a high degree of adaptability to various market conditions.

The strategy is based on a hybrid approach that combines two popular and time-tested techniques.:

1. GRID (grid trading): The classic method of averaging a position is by placing a grid of limit orders.

2. DCA (Dollar Cost averaging): Smart position averaging based on signals from external indicators.

However, "Multi Channel GRID & DCA LTF" goes far beyond the simple combination of these two techniques. The strategy includes a number of unique and innovative features, such as cascading MultiGRID grids for dealing with extreme volatility, Channel Mode range trading mode for profiting from sideways movement, and Low Time Frame analysis (LTF) to achieve surgical accuracy in backtesting. Deep customization options for risk management, capital, take profits, and stop losses allow you to configure a strategy for almost any trading style, asset, and timeframe.

The basic idea: How does it work?

Let's take a detailed look at each of the key concepts embedded in the logic of the strategy.

1. GRID — Automatic placement of buy and sell orders at certain price intervals.

This is a fundamental mode of operation. Its main goal is to systematically improve the average entry price for a position if the market is going against you.

* The principle of operation: After opening the base (first) order (`BO`), the strategy automatically places a series of pending limit orders (here they are called "safety orders" or "SO") at certain price intervals. For a long position, orders are placed below the entry price, and for a short position, orders are placed higher.

* Target: When the price moves against an open position, it consistently hits and executes safety orders. Each such execution adds additional volume to the position at a more favorable price, thereby shifting the overall average entry price (`position_avg_price') closer to the current market price. This means that a much smaller corrective movement will be required to gain ground.

* Flexibility: You have full control over the geometry of the grid: the number of safety orders, the percentage distance between them (`SO Step`), and you can even set a coefficient that will increase this step for each subsequent order (`SO Multiplier`), creating an expanding grid.

2. DCA (Signal Averaging) — Smart Averaging

This mode adds an additional layer of analysis to the averaging process. Instead of just buying/selling at the set price levels, the strategy waits for a confirmation signal.

* Working principle: You can connect any external indicator (for example, RSI, CCI, or even your own complex signal system) to the strategy, which outputs numerical values. As standard, 1 is used for a long signal, and -1 is used for a short signal. The strategy will place the next averaging order only at the moment when it receives the appropriate signal.

* Goal: To average a position not just during a fall (or a rise for a short), but at the moments that your main trading system considers the most favorable for this. This allows you to avoid "catching falling knives" and enter only if there are good reasons.

3. Hybrid Mode (GRID+DCA) is the best of the previous two modes

This mode is designed for maximum filtering and control. It requires two conditions to be fulfilled simultaneously.

* Working principle: The safety order will be executed only if the price has reached the calculated grid level and a confirmation signal has been received from your external indicator. If a confirmation signal is received from an external indicator, the next calculated grid level activates the limit order.

* Goal: To create the most reliable averaging system that protects against premature entries and requires double confirmation (both by price and indicator) before increasing the position size.

4. MultiGRID — Adaptation to extreme volatility

This is one of the most powerful and unique features of a strategy designed to survive and make a profit in the face of strong, protracted trends or "black swans".

* The problem it solves: The usual grid of orders has a limited depth. If the price goes beyond the last safety order, the strategy loses the opportunity to average and becomes vulnerable.

* The principle of operation: The MultiGRID function allows you to create "cascades" — several grids following one another. When all the orders of the first grid are executed, the strategy does not stop. Instead, she can activate the second, third (and so on) a grid of orders. The new grid can be activated by one of two triggers:

1. Offset: The new grid is activated when the price passes another set percentage deviation from the last executed order.

2. Signal: The new grid is activated when a signal is received from an external indicator.

* Goal: To significantly expand the working range of the strategy. This allows it to adapt to strong market movements that would "break" the usual grid, and continue to effectively average a position at a much greater depth of decline or growth.

5. Channel Mode — Trading in the range

This feature turns a standard averaging strategy into a machine for "farming" profits within a price channel that is formed during a sideways market movement.

* The problem it solves: In the standard grid strategy, after partially closing a take profit position, the volume of this part "leaves" the trade until the deal is fully closed. You are missing the opportunity to reuse this capital.

* Operating principle: When Channel Mode is enabled, the following happens. Suppose the price went against you, executed several safety orders, and then turned around and reached one of the partial take profits. At this point, the strategy is:

1. Fixes the profit, as it should be.

2. Instantly places a new limit order to buy (or sell for a short) at exactly the same price level where the last triggered safety order was executed. The volume of this order is equal to the volume of the part that was just closed for take profit.

3. If the price goes down again and executes this "repeat" order, the strategy immediately sets a corresponding take profit for it at the level where the previous profit was taken.

* Goal: To create a continuous buy-sell cycle within the local range (channel). The lower limit of the channel is the price of the last averaging, and the upper limit is the price of a partial take profit. This allows you to repeatedly profit from sideways price fluctuations, without waiting for the full closure of the main, large transaction.

6. LTF (Lower Timeframe Analysis) — Surgical precision of backtesting

This feature is critically important for obtaining reliable results during historical testing (backtesting) of grid strategies.

* The problem it solves: The standard testing mechanism in TradingView has a serious limitation. Working, for example, on a 4-hour chart, he sees only 4 candle points: Open, High, Low and Close. He does not know in what order the price moved within these 4 hours. He could have touched High first and then Low, or vice versa. For grid strategies, this is fatal — the engine can show that a take profit has been executed, although in reality the price first went down, collected the entire grid of orders and only then turned around.

* How it works: When you turn on the LTF mode, the strategy for each candle on your main chart (for example, 4H) requests and analyzes all candles from the lower timeframe you specified (for example, 1-minute). Then it virtually trades the entire price path for these minute candles, executing orders, take profits and stop losses in the sequence in which they would occur in reality. It works in the single take profit mode of the Grid strategy.

* Goal: To provide the most realistic and reliable backtest that reflects the real dynamics of the market. This allows you to avoid false expectations and accurately assess the potential performance of the strategy.

// ------------------------

Part 2: Detailed description of the strategy settings

This section is your main guide to all the switches and options available in the strategy. Understanding each setting is the key to unlocking the full potential of this powerful tool.

1. 🛡️ Risk Management 🛡️

This group contains fundamental parameters that determine the basic logic of risk management and the geometry of grid orders.

* Strategy type: Determines the direction of transactions.

* Long: The strategy will only open long positions (buy).

* Short: The strategy will only open short positions (sell).

* Both: The strategy will work both ways, opening long or short depending on the incoming signal.

* SO Count: Sets the maximum number of Safety (averaging) Orders (SO) that the strategy will place within the same grid. If you have MultiGRID enabled, this number applies to each individual grid.

* SO Step (%): This is the base percentage deviation from the entry price at which the first safety order will be placed. For example, at a value of 0.5, the first SO in a long trade will be placed 0.5% lower than the opening price of the base order.

* SO Multiplier: A coefficient that exponentially increases the step for each subsequent safety order. This allows you to create an expanding grid where averaging orders are placed further and further apart, which is effective with strong and accelerating price movements.

* *The step formula for the nth order*: Step(N) = (SO Step) * (SO Multiplier ^(N-1)).

* If the value is 1, all steps will be the same.

* With a value of 1.6, the step of the second SO will be 1.6 times larger than the first, the step of the third will be 1.6 times larger than the second, and so on.

* 1️⃣ TP/SL: These are simplified settings for quick configuration. They allow you to turn on/off the main take profit and stop loss and set basic percentage values for them. More detailed settings for these parameters can be found in the relevant sections below.

// ------------------------

2. 💰 Money Management 💰

Everything related to position size, leverage, and capital is configured here.

* Volume BO (Base Order): Determines the size of the trade's opening order.

* Volume BO: A fixed amount in the quote currency (for example, in USDT).

* USDT (check mark): Manages the information in the comments to the orders. If enabled, the volume of orders in USDT will be displayed in the comments. This is convenient for visual analysis and for sending the amount of USDT by the placeholder {{strategy.order.comment}} via webhooks when connecting the strategy to the exchange or trading terminals.

* or % of deposit: The amount calculated as a percentage of the available capital of the strategy. The check mark to the right of this field enables this mode. Important: using a percentage activates the effect of compounding (compound interest), as the amount of each new transaction will be automatically recalculated based on the current capital (initial capital + profit/loss). If enabled, the percentage of orders will be displayed in the comments. This is convenient for visual analysis and for sending percentages on the placeholder {{strategy.order.comment}} via webhooks when connecting the strategy to the stock exchange, trading terminals, or creating Copy trading.

* Martingale: The coefficient applied to the volume of orders. It increases the size of each subsequent insurance order compared to the base one.

* Volume formula for the nth SO: Volume SO (N) = (Volume BO) * (Martingale^N).

* With a value of 1.2, the volume of the first SO will be 1.2 times greater than the base, the second — 1.44 times (`1.2 * 1.2`) and so on.

* Leverage: Specify the size of your leverage. This parameter is used exclusively for calculating and displaying the approximate liquidation price. It does not affect the size of positions, but it helps to visually assess the risks.

* Liquidation: Enables or disables the calculation and display of the liquidation line on the chart.

* Margin type: Allows you to select a method for calculating the liquidation price, simulating the logic of exchanges:

* Isolated: The liquidation price is calculated based on the size and leverage of the current open position only.

* Cross: The calculation simulates using the entire available balance to maintain a position. In the strategy, the liquidation price is calculated as the level at which the loss on the current transaction is equal to the current capital.

* Commission (%): Specify the percentage of your exchange's commission per transaction. The correct value of this parameter is crucial for obtaining realistic backtest results.

// ------------------------

3. 🕸️ Grid Management 🕸️

This group is responsible for the logic of safety orders and advanced mechanics such as Channel Mode and MultiGRID.

* SO Type: Defines the logic of placing averaging orders.

* GRID: Classic grid. All safety orders are placed in advance as limit orders.

* DCA: Signal averaging. The strategy is waiting for a signal from an external indicator to place a market averaging order.

* GRID+DCA: Hybrid. The strategy waits for a signal, and if it arrives, places a limit order at the appropriate price level of the grid or executes a market order if the signal has arrived below the limit order level.

* Signal for SO: A data source (indicator) that will be used for signals in DCA and GRID+DCA modes.

* ↔️ Channel Mode: When this option is enabled, the strategy tries to trade in a sideways range. After partially closing a take profit position, it immediately places a limit order for re-entry at the price of the last triggered safety order. This creates a buy-sell cycle within the local channel.

* Best Price Only: This filter adds an additional condition for averaging in DCA and MultiGRID modes (when it operates on a signal). The next averaging order or a new grid will be activated only if the current price is more favorable (lower for long, higher for short) than the price of the previous entry.

* 🧩 MultiGRID ⮕ Enables cascading grid mode.

* Grid Count: The total number of grids that can be activated sequentially.

* Offset: Percentage deviation from the price of the last order of the previous grid. When this margin is reached, the following grid of orders is activated (this mode does not require a signal).

* Or signal: Allows you to use the signal from an external indicator as a trigger to activate the next grid. The checkmark on the right turns on this mode.

// ------------------------

4. 🎯 Entry and Stop 🎯

This group of settings allows you to fine-tune the conditions for starting a new trade and all aspects related to protective stop orders, including the complex mechanics of trailing and managing SL after partial take profits.

* 🎯 Signal: A data source (indicator) that will be used to determine when to enter a trade. The strategy expects a value of 1 for the start of a long trade and -1 for a short trade.

* Min Bars: Sets the minimum number of candles that must pass from the moment of opening the previous trade to the moment of opening the next one. A value of 0 disables this filter. This is a useful tool to prevent overly frequent entries in a "noisy" market.

* Non-stop: If this option is enabled, the strategy ignores the Entry Signal and opens a new trade immediately after closing the previous one (taking into account the Min Bars filter, if it is set). This turns the strategy into a constantly working mechanism that is always on the market.

* 🛑 SL Type: Defines the base price from which the stop loss percentage will be calculated. The stop loss in the first section must be enabled for this block of settings to work.

* From the entry point: SL is always calculated from the opening price of the very first base order. It remains static throughout the entire transaction unless it is moved by other functions.

* From breakeven line: SL is dynamically recalculated and shifted each time a safety order is executed. It always follows the average price of the position, being at a given percentage distance from it.

* From last executed SO: SL is recalculated from the price of the last executed order, whether it is a base or a safety order.

* From last SO: SL is calculated from the price of the most recent possible safety order in the grid. This is usually the most remote and conservative type of SL.

* Trailing SL Type: Defines the algorithm by which the stop loss will move after its activation.

* Standard: Classic trailing. After activation, SL will follow the price at a fixed distance.

* ATR: SL will follow the price at a distance equal to the value of the ATR indicator multiplied by the specified multiplier.

* External Source: SL will follow any selected line of the third-party indicator.

* Period and Multiplier: Common parameters for all types of trailing.

* Source: The source of the line for the trailing SL of the third-party indicator.

* Trailing SL after entry: The mode of activation of the trailing SL after entering the transaction

* SL management after TP (sections 1️⃣, 2️⃣, 3️⃣): These three blocks allow you to create a complex stop loss management logic as profits are recorded.

For each take profit level (TP1, TP2, TP3), you can configure:

* SL BE / SL TP1 / SL TP2: When the corresponding TP is reached, the stop loss will be moved to the breakeven point (for TP1), to the TP1 price level (for TP2) or to the TP2 price level (for TP3).

* Trailing SL: When the corresponding TP is reached, the trailing stop loss is activated according to the settings above.

* By ↔️ Signal: A very powerful option. If it is enabled, the above action (SL transfer or trailing activation) will occur when the opposite trading signal is received from an external indicator. This allows you to protect profits or reduce losses if the market turns sharply, even before reaching the target.

* SL Delay ⮕ Allows you to delay the activation of the stop loss.

* Number of Bars: The Stop loss will be physically placed on the market only after the specified number of candles has passed since entering the trade. This can help to avoid "taking out" the stop with a random short movement (squiz) immediately after opening a position.

* SL Block: Unique defensive mechanics for trading both ways (`Strategy Type: Both`).

* Number of SL: If the strategy receives the specified number of stop losses in a row in one direction (for example, 2 stops long), it temporarily blocks the opportunity to open new trades in that direction.

* Lock Reset mode:

* By direction: The lock is lifted if a profitable trade is closed in the allowed direction or if a stop loss is triggered in the opposite direction.

* First profit: The lock is lifted after closing any profitable transaction, regardless of its direction.

// ------------------------

5. ✅ Take Profit ✅

This group of settings provides comprehensive control over profit taking, from a simple take profit to a complex system of partial closures and trailing.

* ✅ TP Type: Defines the base price for calculating the percentage deviation of the take profit.

* From entry point: TP is calculated from the base order price.

* From breakeven line: TP dynamically follows the average position price.

* From last executed SO: TP is calculated from the price of the last executed order.

* Filters for closing on signal

* Only ➕: If TP is triggered by a signal, the deal will be closed only if it is in the black relative to the average price.

* Or >TP: If TP is triggered by a signal, the trade will be closed only if the closing price is better than (or equal to) the estimated price of this TP.

* TP type of trailing: Yes, take profit has a trailing too! It works differently than the SL trailing.

* Standard / ATR: After the price touches the "virtual" TP level, the trailing is activated. He does not place a stop order, but begins to move away from the price, dynamically moving the limit order to close further and further in the profitable direction, allowing him to collect the maximum from the impulse movement.

* External Source: TP will follow any selected line of the third-party indicator.

* Period and Multiplier: Parameters for calculating the trailing margin TP.

* Source: The source of the line for the trailing TP of the third-party indicator.

* TP level settings (sections 1️⃣, 2️⃣, 3️⃣, 4️⃣): The strategy supports up to four independent take profit levels, which allows for a flexible system of partial commits.

For each level, you can set:

* TP: Enable the level and set its percentage deviation from the base price.

* Size: What percentage of the current position will be closed when this level is reached. For the last active TP, this parameter is ignored, and 100% of the remaining position is closed.

* Trailing TP: Enable the above-described trailing mechanism for this particular level.

* Signal: Enable closing based on the signal from the external indicator for this level.

* Or take: If both the closing on the signal and the limit order are enabled, then whatever comes first will work.

* After SO: Activate this TP level only after the specified number of safety orders has been executed. This allows you to set closer targets for riskier (deeply averaged) positions.

// ------------------------

6. 🔬 GRID and MultiGrid Analysis on Lower TFs (LTF) 🔬

This group activates one of the most important functions for accurate testing of grid strategies.

* Enable LTF Calculation ⮕ The main switch of the analysis mode on the lower timeframes.

* Timeframe selection: A drop-down list where you can select a timeframe for detailed analysis. For example, if your main schedule is 1 hour, you can select 1 minute here. The strategy will emulate the trading of minute candles within each hour candle.

❗️Important: As mentioned in the first part, the use of this mode is critically necessary to obtain realistic backtest results, especially for strategies with a dense grid of orders. Without it, the results may be overly optimistic and not reflect the real dynamics of the market. It should be remembered that TradingView imposes a limit on the number of intra-bars (minor TF bars) that can be requested. This is usually about 100,000 bars.

// ------------------------

7. 🕘 Backtest Date Range 🕘

This group allows you to focus testing on a specific historical period.

* Limit Date Range: Enables date filtering.

* Start time: The date and time when the strategy will start analyzing and opening deals.

* End time: The date and time after which the strategy will stop opening new deals and complete testing.

// ------------------------

8. 🎨 Visualization 🎨

All the options responsible for the appearance and information content of the chart are collected here.

* Show PnL labels: Enables/disables the display of text labels with the result (profit/loss) after closing each trade.

* Statistics Table: Enables/disables the main dashboard with detailed statistics on the results of the backtest.

* Strategy Settings Table: Enables/disables an additional panel that summarizes all the key parameters of the current configuration.

* Monthly Profit Table: Enables/disables a table with a breakdown of percentage returns by month and year.

* Table settings: For each of the three tables, you can individually adjust the Text size and Table Position on the screen to position them as conveniently as possible.

* Decimal places: Defines how many decimal places will be displayed in numeric values in tables and on labels.

// ------------------------

9. ✉️ Webhook Settings ✉️

This group is intended for traders who want to automate trading on strategy signals using third-party services and exchanges (for example, 3Commas, WunderTrading, Cryptorobotics, Cryptohopper, Bitsgap, Binance, ByBit, OKX, Pionex, Bitget or proprietary solutions).

For each key event in the strategy, there is a separate switch and a text field:

* Webhook for Open: Enable and set a message for the webhook that will be sent when the base order is opened.

* Webhook for Averaging: A message sent when executing any insurance order.

* Webhook for Take Profit: A message sent when closing on take profit (including partial ones).

* Webhook for Stop-Loss: A message sent when a stop loss is closed.

You can insert a JSON code or any other message format that your service requires for automation into the text fields. The strategy supports special placeholders (for example, `{{strategy.order.alert_message}}`), which allow you to dynamically insert the necessary data into the message, such as the amount of USDT or the percentage of the deposit for entry, averaging and take profit orders.

Valid H/L Strategy Tester with MFE/MAE Analytics

## Overview

A data-driven trading indicator that identifies valid high/low price levels and provides statistical insights through Maximum Favorable Excursion (MFE) and Maximum Adverse Excursion (MAE) analytics. Make informed trading decisions based on historical price behavior rather than guesswork.

## Key Features

### 🎯 Smart Pattern Recognition

- Automatically detects valid highs and lows with confirmation system

- Color-coded candles and lines for clear visual identification

- Inside/Outside print filtering for higher probability setups

### 📊 Statistical Analytics

- Analyzes up to 500 historical setups for MFE/MAE calculations

- 1-hour and 3-hour timeframe data with percentile-based targets (20th, 50th, 80th)

- Real-time performance tracking with comprehensive statistics table

### ⚙️ Flexible Strategy Options

**Entry Methods:** Confirmation-based or MAE percentile entries

**Take Profit:** MFE-based, fixed points, percentage, or R:R ratio targets

**Risk Management:** Multiple stop loss types with position sizing controls

### 🕐 Advanced Time Filtering

- Session filters (Asia, London, New York)

- Individual hourly controls (24-hour precision in ET)

- Pre-configured for optimal NY trading hours (9 AM - 2 PM)

### 📈 Visual Dashboard

- MFE target lines (blue) and MAE risk lines (orange)

- Customizable colors, styles, and line weights

- Statistics table showing daily/hourly/weekly performance breakdowns

## How It Works

1. **Pattern Detection** - Scans for valid high/low formations using price structure and gap behavior

2. **Statistical Analysis** - Calculates historical MFE/MAE percentiles from past setups

3. **Trade Framework** - Executes entries/exits based on your configuration with real-time performance tracking

## Ideal For

- **Day/Swing Traders** seeking data-driven entry/exit levels

- **Risk Managers** wanting historical drawdown data for stop placement

- **Performance Trackers** needing detailed analytics across timeframes and sessions

- **Flexible Strategies** - adapts to scalping, day trading, or swing trading styles

## Quick Setup

1. Select analysis timeframe (default: 5-minute)

2. Choose entry method and exit strategy

3. Enable MFE/MAE analytics display

4. Apply session/hourly filters

5. Customize visual elements and table settings

Transform your trading from guesswork to statistical precision with historical price behavior insights.

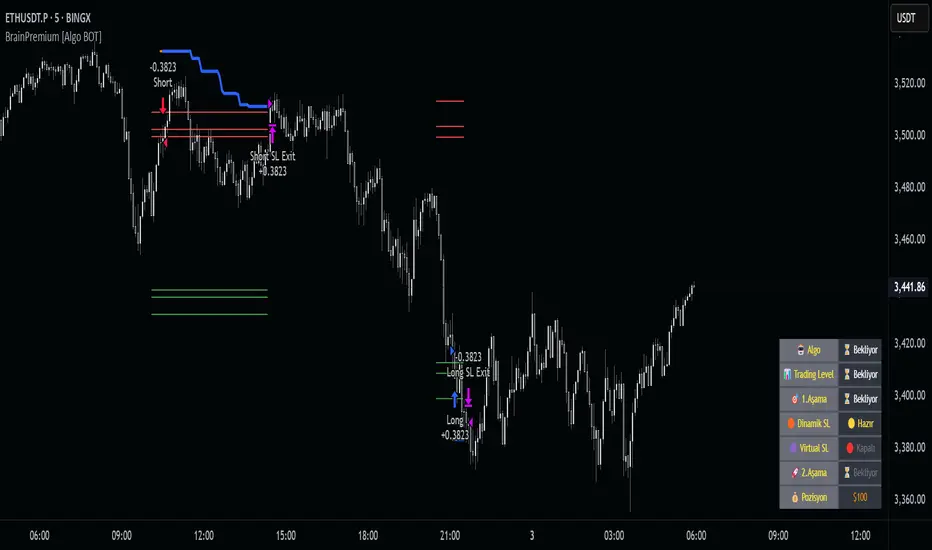

Brain Premium [ALGO]💡 Brain Premium ALGO

Brainpremium ALGO is a strategy algorithm that analyzes a two-phase regional liquidity structure and only opens positions on price breakouts occurring within these liquidity zones.

This system is developed based on the market experience of manual traders and automatically executes trade decisions using AI-like rules and specific triggers.

💡 Two-Phase Liquidity-Based Entry Strategy

This strategy operates by detecting liquidity sweep zones and confirmed reversal signals:

🔹 Phase 1 – Liquidity Sweep:

Price is expected to sweep areas where equal highs/lows or liquidity clusters exist. These zones are considered potential reversal levels.

🔹 Phase 2 – Confirmed Entry:

After liquidity is swept, entries are triggered only by confirmed reversal signals such as structural breaks, inside bars, or breakouts in the opposite direction.

✅ Entries are triggered only when liquidity and reversal confirmation occur simultaneously.

🎯 This approach targets high-probability, low-risk trades.

⚙️ Key Features

🔍 Dynamic Liquidity Detection — Automatically identifies liquidity zones.

🧩 Modular Entry Options (1–2–3) — Allows opening positions via different strategy paths.

🛡️ Dynamic Stop Loss System — Stop Loss adjusts as price moves favorably.

📈 Advanced Risk Management — Adjustable Take Profit, Stop Loss, leverage, balance, and mode.

🔔 JSON Alert Support — Connects to platforms like BingX via webhook.

🧾 Information Panel — Displays real-time trade data and strategy status.

📊 Backtest & Default Settings

Strategy tests are conducted with realistic and sustainable parameters:

Parameter Value

Trading Balance: $100 (%10 of total wallet)

Leverage: 10x

Stop Loss: 1%

Take Profit Type : High TP (optional: Low and Risky also available)

Entry Option 1 (optional: 2 and 3 also available)

Mode: NORMAL

Commission 0.05%

Dynamic Stop Loss: Enabled

Timeframe: 5 minute

Pair ETH/USDT

Duration: 30 days

🧭 Usage Instructions

Add Brain Premium ALGO to your TradingView chart.

Set position size, leverage, and SL/TP levels from the settings panel.

Select entry option (1, 2, or 3).

Activate backtesting and alert systems to monitor the strategy.

⚠️ Disclaimer

This strategy is not financial advice. Past performance does not guarantee future results. Trade only with capital you can afford to risk and always test thoroughly in a demo environment first.

Pro Reversal Strategie - FinalCore Functionality Description

The "Pro Reversal Strategy" script is a comprehensive and highly customizable trading system for TradingView. Its core idea is based on a mean-reversion strategy, which aims to capitalize on price extremes where the price is likely to revert to its statistical mean. This script ist full AI generated. There ist no support and no financial advice.

To identify entry points, the script combines classic indicators like the RSI (to detect overbought and oversold conditions) and Bollinger Bands (to measure volatility extremes).

However, the script's strength lies in its confluence logic: a simple RSI or Bollinger Band signal is not enough to trigger a trade. Instead, a series of filters are applied to enhance the quality of the trade signals. These include:

Trend Filter: Trades are only taken in the direction of the higher-level trend (defined by a 200-period Moving Average).

Volatility and Volume Filter: ADX and volume analysis ensure that the market has sufficient momentum for a move.

Market Structure Analysis: Concepts like Fair Value Gaps (FVG), liquidity zones, and the Volume Profile (VRVP/POC) are used to place trades in high-probability zones.

Momentum Filter: Special "Vector Candles" confirm the strength of buyers or sellers at the moment of the signal.

Furthermore, the script offers advanced features for risk and trade management, including automatic position sizing based on a percentage risk and dynamic exit strategies like a breakeven stop and a trailing stop-loss (Chandelier ATR).

A detailed info panel visualizes all key metrics in real-time directly on the chart. Thanks to its versatile configuration options, the script can be adapted for various trading styles, including swing trading, day trading, and scalping.

Core Strategies & Filters (English)

Here is a breakdown of the specific strategies and confirmation filters used within the script:

RSI Mean Reversion: Uses the Relative Strength Index (RSI) to identify overbought (> rsiSellShort) and oversold (< rsiBuyLong) conditions, which serve as the primary trigger for a potential price reversal.

Bollinger Bands (BB) Volatility Filter: Trades are confirmed when the price touches or exceeds the outer Bollinger Bands. This indicates a move to a statistical extreme in terms of volatility, reinforcing the reversal thesis.

Trend Filter (200 SMA): Ensures that long trades are only considered in a general uptrend (price > SMA 200) and short trades in a downtrend (price < SMA 200), preventing trades against the dominant market direction.

ADX Trend Strength Filter: Utilizes the Average Directional Index (ADX) to confirm that a market is trending with sufficient strength. Trades are filtered out during weak or non-trending phases (adx < adxThreshold).

Volume Profile (VRVP / POC): Analyzes volume at specific price levels to identify high-volume nodes (Point of Control - POC). This acts as a filter to avoid entering trades directly into a zone of strong support or resistance.

Vector Candle Filter: Identifies "Vector Candles" – large, high-volume candles that close strongly near their high (bullish) or low (bearish). This custom filter confirms strong conviction behind the initial reversal signal.

Market Structure (FVG & Liquidity): Incorporates advanced price action concepts. It looks for entries after a liquidity zone above a previous high/low has been tapped (Liquidity Grab) or when price enters a Fair Value Gap (FVG), adding a layer of institutional trading logic.

Chart Pattern Recognition: Optionally identifies classic chart patterns like "W-Patterns" (Double Bottom), "M-Patterns" (Double Top), and Ascending Triangles to provide additional visual confirmation for traders.

Position Sizing (Risk %): Automatically calculates the trade size based on a user-defined percentage of the total equity (riskPct) and the distance to the stop-loss, ensuring consistent risk management for every trade.

Dynamic Exit Management: Implements advanced exit strategies beyond a fixed take-profit. This includes moving the stop-loss to Breakeven after a certain risk-to-reward ratio is met and using a Trailing Stop-Loss (e.g., Chandelier ATR) to lock in profits as a trade develops.

NY Opening Range Breakout - MA StopCore Concept

This strategy trades breakouts from the New York opening range (9:30-9:45 AM NY time) on intraday timeframes, designed for scalping and day trading.

Setup Requirements

Timeframe: Works on any timeframe under 15 minutes (1m, 2m, 3m, 5m, 10m)

Session: New York market hours

Range Period: 9:30-9:45 AM NY time (15-minute opening range)

Entry Rules

Long Entries:

Wait for a candle to close above the opening range high

Enter long on the next candle (before 12:00 PM NY time)

Must be above moving average if using MA-based take profit

Short Entries:

Wait for a candle to close below the opening range low

Enter short on the next candle (before 12:00 PM NY time)

Must be below moving average if using MA-based take profit

Risk Management

Stop Loss:

Long trades: Opening range low

Short trades: Opening range high

Take Profit Options:

Fixed Risk Reward: 1.5x the range size (customizable ratio)

Moving Average: Exit when price crosses back through MA

Both: Whichever comes first

Key Features

Trade Direction Options:

Long Only

Short Only

Both directions

Moving Average Filter:

Prevents entries that would immediately hit stop loss

Uses EMA/SMA/WMA/VWMA with customizable length

Acts as dynamic support/resistance

Time Restrictions:

No entries after 12:00 PM NY time (customizable cutoff)

One trade per direction per day

Daily reset of all variables

Visual Elements

Red/green lines showing opening range

Purple line for moving average

Entry and breakout signals with shapes

Take profit and stop loss levels plotted

Information table with current status

Strategy Logic Flow

Morning: Capture 9:30-9:45 range high/low

Wait: Monitor for breakout (previous candle close outside range)

Filter: Check MA condition if using MA-based exits

Enter: Trade on next candle after breakout

Manage: Exit at fixed TP, MA cross, or stop loss

Reset: Start fresh next trading day

This is a momentum-based breakout strategy that capitalizes on early market volatility while using the opening range as natural support/resistance levels.

G-Bot v3Overview:

G-Bot is an invite-only Pine Script tailored for traders seeking a precise, automated breakout strategy. This closed-source script integrates with 3Commas via API to execute trades seamlessly, combining classic indicators with proprietary logic to identify high-probability breakouts. G-Bot stands out by filtering market noise through a unique confluence of signals, offering adaptive risk management, and employing advanced alert deduplication to ensure reliable automation. Its purpose-built design delivers actionable signals for traders prioritizing consistency and efficiency in trending markets.

What It Does and How It Works:

G-Bot generates trade signals by evaluating four key market dimensions—trend, price action, momentum, and volume—on each 60-minute bar. The script’s core components and their roles are:

Trend Detection (EMAs): Confirms trend direction by checking if the 5-period EMA is above (bullish) or below (bearish) the 6-period EMA, with the price positioned accordingly (above the 5-period EMA for longs, below for shorts). The tight EMA pairing is optimized for the 60-minute timeframe to capture sustained trends while minimizing lag.

Price Action Trigger (Swing Highs/Lows): Identifies breakouts when the price crosses above the previous swing high (for longs) or below the previous swing low (for shorts), using a period lookback to focus on recent price pivots. This ensures entries align with significant market moves.

Momentum Filter (RSI): Validates breakouts by requiring RSI to fall within moderated ranges. These ranges avoid overbought/oversold extremes, prioritizing entries with balanced momentum to enhance trade reliability.

Volume Confirmation (3-period SMA): Requires volume to exceed its 3-period SMA, confirming that breakouts are driven by strong market participation, reducing the risk of false moves.

Risk Management (14-period ATR): Calculates stop-loss distances (ATR) and trailing stops (ATR and ATR-point offset) to align trades with current volatility, protecting capital and locking in profits.

These components work together to create a disciplined system: the EMAs establish trend context, swing breaks confirm price momentum, RSI filters for optimal entry timing, and volume ensures market conviction. This confluence minimizes false signals, a critical advantage for hourly breakout trading.

Why It’s Original and Valuable:

G-Bot’s value lies in its meticulous integration of standard indicators into a non-standard, automation-focused system. Its unique features include:

Curated Signal Confluence: Unlike generic breakout scripts that rely on single-indicator triggers (e.g., EMA crossovers), G-Bot requires simultaneous alignment of trend, price action, momentum, and volume. This multi-layered approach, reduces noise and prioritizes high-conviction setups, addressing a common flaw in simpler strategies.

Proprietary Alert Deduplication: G-Bot employs a custom mechanism to prevent redundant alerts, using a 1-second minimum gap and bar-index tracking. This ensures signals are actionable and compatible with 3Commas’ high-frequency automation, a feature not found in typical Pine Scripts.

Adaptive Position Sizing: The script calculates trade sizes based on user inputs (1-5% equity risk, max USD cap, equity threshold) and ATR-derived stop distances, ensuring positions reflect both account size and market conditions. This dynamic approach enhances risk control beyond static sizing methods.

3Commas API Optimization: G-Bot generates JSON-formatted alerts with precise position sizing and exit instructions, enabling seamless integration with 3Commas bots. This level of automation, paired with detailed Telegram alerts for monitoring, streamlines the trading process.

Visual Clarity: On-chart visuals—green triangles for long entries, red triangles for shorts, orange/teal lines for swing levels, yellow circles for price crosses—provide immediate insight into signal triggers, allowing traders to validate setups without accessing the code.

G-Bot is not a repackaging of public code but a specialized tool that transforms familiar indicators into a robust, automated breakout system. Its originality lies in the synergy of its components, proprietary alert handling, and trader-centric automation, justifying its invite-only status.

How to Use:

Setup: Apply G-Bot to BITGET’s BTCUSDT.P chart on a 60-minute timeframe.

3Commas Configuration: Enter your 3Commas API Secret Key and Bot UUID in the script’s input settings to enable webhook integration.

Risk Parameters: Adjust Risk % (1-5%), Max Risk ($), and Equity Threshold ($) to align position sizing with your account and risk tolerance.

Webhook Setup: Configure 3Commas to receive JSON alerts for automated trade execution. Optionally, connect Telegram for detailed signal notifications.

Monitoring: Use on-chart visuals to track signals:

Green triangles (below bars) mark long entries; red triangles (above bars) mark shorts.

Orange lines show swing highs; teal lines show swing lows.

Yellow circles indicate price crosses; purple crosses highlight volume confirmation.

Testing: Backtest G-Bot in a demo environment to validate performance and ensure compatibility with your trading strategy.

Setup Notes : G-Bot is a single, self-contained script for BTCUSDT.P on 60-minute charts, with all features accessible via user inputs. No additional scripts or passwords are required, ensuring compliance with TradingView’s single-publication rule.

Disclaimer: Trading involves significant risks, and past performance is not indicative of future results. Thoroughly test G-Bot in a demo environment before deploying it in live markets.

Full setup support will be provided

Shockwave⚡️ Shockwave – Precision Momentum Strategy

🔹 Purpose

Shockwave is a precision-engineered trend and momentum strategy designed for aggressive, high-conviction trades. Built for volatile markets like crypto, this system enters only when trend, volume, and momentum are fully aligned — then exits intelligently using layered profit targets and trend weakening logic.

It filters out false breakouts, traps, and low-quality setups using advanced multi-factor confirmation. Ideal for trend-following traders who want cleaner signals, no repainting, and adaptive position handling.

🔹 Indicator Breakdown

1️⃣ ZLEMA + Gradient Filter (Trend Core)

Defines the trend using a Zero Lag EMA (ZLEMA) for responsiveness.

Gradient slope confirms acceleration or weakening in trend direction.

Uptrend: ZLEMA is rising and slope > 0.

Downtrend: ZLEMA is falling and slope < 0.

2️⃣ Smoothed CCI (Momentum Confirmation)

Uses ZLEMA as the source for CCI to avoid noise.

Bullish momentum: CCI rising above 0.

Bearish momentum: CCI falling below 0.

Filters out chop and premature entries.

3️⃣ Volume Spike Filter

Median-based filter confirms breakout volume integrity.

Requires volume > 1.5x median of previous candles.

Avoids low-volume whipsaws.

4️⃣ Vortex Indicator (Trend Strength Confirmation)

Confirms directional conviction by comparing VI+ vs VI–.

Long: VI+ > VI– and threshold difference is met.

Short: VI– > VI+ and trend strength is validated.

5️⃣ Wick Trap Filter (Reversal Trap Detection)

Blocks entries on manipulative upper/lower wick patterns.

Longs rejected if upper wick > 1.5× body and close is weak.

Shorts rejected if lower wick > 1.5× body and close is strong.

🔹 Strategy Logic & Trade Execution

✅ Entry Conditions

A trade is entered only when all the following align:

ZLEMA trend direction is confirmed.

CCI momentum matches the trend.

Volume spike confirms participation.

Vortex difference meets strength threshold.

No wick trap is present.

✅ Exit Conditions

TP1: 50% of the position is closed at the first profit level.

TP2: Remaining 50% is closed at the second target.

Weak Trend Exit: If ZLEMA slope flips against the trade, the position is closed early.

A 1-bar cooldown delay is enforced after closing to prevent same-bar reentry.

🔹 Take-Profit System

TP1: 50% close at +2% for longs / –2% for shorts

TP2: Full close at +4% for longs / –4% for shorts

Limit orders are used for precise profit-taking

TP1/TP2 status is tracked and displayed in the live dashboard

🔹 Risk Management (Important)

🚫 This strategy does not include a stop-loss by default.

Trades are exited using trend reversal detection or TP targets.

💡 Suggested risk controls:

Add a manual stop-loss based on recent swing high/low

Use appropriate position sizing based on volatility

Apply the strategy in strong trending environments

🔹 Default Backtest Settings

Initial Capital: $1,000

Position Size: 10% of equity per trade

Commission: 0.05%

Slippage: 1

Strategy Date Filter: Adjustable (default: 2023–2029)

🔹 How to Use Shockwave

Apply to any chart (best results on 1H or higher).

Review backtest performance.

Adjust take-profit percentages or thresholds as needed.

Use in strongly trending markets — avoid sideways ranges.

Add your own stop-loss if desired.

⚠️ Disclaimer

This strategy is for educational and informational purposes only. It is not financial advice. Trading involves risk, and past performance does not guarantee future results. Always test thoroughly and manage your own risk.

🚀 Why Use Shockwave?

✔ Multi-layer confirmation for high-quality entries

✔ Non-repainting logic for backtest/live consistency

✔ Adaptive trend/momentum filtering

✔ Dual profit targets for smart trade management

✔ Visual dashboard with live tracking

Daily Breakout + Daily Shadow By RouroThis script is a Pine v5 strategy designed to detect daily candle body breakouts and execute them on any intraday timeframe, while also providing:

Daily Data Retrieval

Using request.security(..., "D", ...) it fetches the OHLC and timestamp of the daily candle, regardless of the chart’s current timeframe.

Calculation of Yesterday’s and Day-Before-Yesterday’s Bodies

b1High and b1Low → the high/low of yesterday’s daily candle body

b2High and b2Low → the high/low of the previous day’s body

Detection of the First Intraday Bar After a New Day

By using ta.change(time("D")), it marks the start of each new trading day.

Drawing the Previous Day’s “Shadow” on the Chart

It overlays a box (box.new) and two wick lines (line.new) with configurable colors and transparency, so you can clearly see the full range of yesterday’s candle on any intraday chart.

Automatic End-of-Day Position Closure

It will automatically close any open position at the start of the next day to avoid unintended rollovers.

Entry Signals

On the very first intraday bar after the daily close:

Long if yesterday’s close broke above the body of the day before yesterday

Short if yesterday’s close broke below the body of the day before yesterday

…which triggers a strategy.entry at the intraday open.

Fully Customizable Stop-Loss and Take-Profit

SL options:

Opposite end of yesterday’s body

Fixed pips from entry

A risk-reward ratio on yesterday’s wick

Optional “safety SL” in fixed pips that overrides the above

TP options:

Fixed pips

Yesterday’s wick extreme (high/low)

Partial exit on the wick (TP1), then second exit (TP2) either:

At a multiplied RR

Or at the daily close (“Close of Day”)

You can also choose to move SL to breakeven after TP1 is hit.

Live Metrics Table

In the upper-right corner it displays in real time:

Start of backtest (date of first trade)

Number of ✅ Winning trades and ❌ Losing trades

Total number of trades

Win rate (%)

Profit Factor

All within a fixed table layout so it never runs out of rows or columns.

TrendSync Pro (SMC)📊 TrendSync Pro (SMC) – Advanced Trend-Following Strategy with HTF Alignment

Created by Shubham Singh

🔍 Strategy Overview

TrendSync Pro (SMC) is a precision-based smart trend-following strategy inspired by Smart Money Concepts (SMC). It combines: Real-time pivot-based trendline detection

Higher Time Frame (HTF) filtering to align trades with dominant trend

Risk management via adjustable Stop Loss (SL) and Take Profit (TP)

Directional control — trade only bullish, bearish, or both setups

Realistic backtesting using commissions and slippage

Pre-optimized profiles for scalpers, intraday, swing, and long-term traders

🧠 How It Works:

🔧 Strategy Settings Image:

beeimg.com

The strategy dynamically identifies trend direction by using swing high/low pivots. When a new pivot forms: It draws a trendline from the last significant pivot

Detects whether the trend is up (based on pivot lows) or down (based on pivot highs)

Waits for price to break above/below the trendline

Confirms with HTF price direction (HTF close > previous HTF close = bullish)

Only then it triggers a long or short trade

It exits either at TP, SL, or a manual trendline break

🛠️ Adjustable Parameters:

Trend Period: Length for pivot detection (affects sensitivity of trendlines)

HTF Timeframe: Aligns lower timeframe entries with higher timeframe direction

SL% and TP%: Customize your risk-reward profile

Commission & Slippage: Make backtests more realistic

Trade Direction: Choose to trade: Long only, Short only, or Both

🎛️ Trade Direction Control:

In settings, you can choose: Bullish Only: Executes only long entries

Bearish Only: Executes only short entries

Both: Executes both long and short entries when conditions are met

This allows you to align trades with your own market bias or external analysis.

📈 Entry Logic: Long Entry:

• Price crosses above trendline

• HTF is bullish (HTF close > previous close)

• Latest pivot is a low (trend is considered up)

Short Entry:

• Price crosses below trendline

• HTF is bearish (HTF close < previous close)

• Latest pivot is a high (trend is considered down)

📉 Exit Logic: Hit Take Profit or Stop Loss

Manual trendline invalidation: If price crosses opposite of the trend direction

⏰ Best Timeframes & Recommended Settings:

Scalping (1m to 5m):

HTF = 15m | Trend Period = 7

SL = 0.5% | TP = 1% to 2%

Intraday (15m to 30m):

HTF = 1H | Trend Period = 10–14

SL = 0.75% | TP = 2% to 3%

6 Hour Trading (30m to 1H):

HTF = 4H | Trend Period = 20

SL = 1% | TP = 4% to 6%

Swing Trading (4H to 1D):

HTF = 1D | Trend Period = 35

SL = 2% | TP = 8% to 12%

Long-Term Investing (1D+):

HTF = 1W | Trend Period = 50

SL = 3% | TP = 15%+

Note: These are recommended base settings. Adjust based on volatility, asset class, or personal trading style.

📸 Testing Note:

beeimg.com

TradingView limits test length to 20k bars (~40 trades on smaller timeframes). To show long-term results: Test on higher timeframes (e.g., 1H, 4H, 1D)

Share images of backtest result in description

Host longer test result screenshots on Imgur or any public drive

📍 Asset Behavior Insight:

This strategy works on multiple assets, including BTC, ETH, etc.

Performance varies by trend strength:

Sometimes BTC performs better than ETH

Other times ETH gives better results

That’s normal as both assets follow different volatility and trend behavior

It’s a trend-following setup. Longer and clearer the trend → better the results.

✅ Best Practices: Avoid ranging markets

Use proper SL/TP for each timeframe

Use directional filter if you already have a directional bias

Always forward test before going live

⚠️ Trading Disclaimer:

This script is for educational and backtesting purposes only. Trading involves risk. Always use risk management and never invest more than you can afford to lose.

Enhanced BarUpDn StrategyEnhanced BarUpDn Strategy

The Enhanced BarUpDn Strategy is a refined price action-based trading approach that identifies market trends and reversals using bar formations. It focuses on detecting bullish and bearish momentum by analyzing consecutive price bars and key support/resistance levels.

Key Features:

✅ Trend Confirmation – Uses a combination of bar patterns and indicators (e.g., moving averages, RSI) to confirm momentum shifts.

✅ Entry Signals – A buy signal is triggered when an "Up Bar" (higher high, higher low) follows a bullish setup; a sell signal when a "Down Bar" (lower high, lower low) confirms bearish momentum.

✅ Enhanced Filters – Incorporates volume analysis and additional conditions to reduce false signals.

✅ Stop-Loss & Risk Management – Uses recent swing highs/lows for stop placement and dynamic trailing stops for maximizing gains.

Kinetik Model [NantzOS]Description:

The Kinetik Model is a strategy that reinterprets the traditional stochastic oscillator to take advantage of momentum instead of the standard overbought/oversold reversal approach. Primarily operating upon zero line crosses, what you observe is the difference between the K and D plots. the first unique feature about this system is that the stochastic calculation has been made "boundless" in order to more accurately gauge the rate of momentum. It doesn't consolidate in upper or lower channels. The second feature is the dataset typically known as %K smoothing is set to a fixed value, the %K length and %D smoothing serve as a customizable length and signal. The third is that it takes trades based on the difference between the fixed %K and customizable %D, a reminder that is your oscillator display. This oscillator versus the traditional stochastic is comparable to the MACD histogram versus the MACD line plots. The fourth feature is that the user dynamically tests the upper and lower thresholds, displayed with a color background on the oscillator, to act as a filtration method. The system won't take shorts if momentum is above the upper threshold and won't take longs if it's performing below the lower threshold. Lastly, this system uses a trailing stop exit strategy, which can be deactivated, and the option to test long only.

Features Summarized:

A reimagined stochastic that operates without fixed boundries, offering flexibility for properly observing momentum.

High and low levels act as extreme zones for highlighting strong trends.

Users can modify data length, signal input, and thresholds from the settings to suit their preferred asset and time frame.

A built-in optional stop-loss mechanism with adjustable sensitivity, enabling tighter or more relaxed risk management.

Includes and optional long only setting and candle coloring with signals.

How to Use:

Navigate to the indicator tab in TradingView to search and apply the Kinetik Model.

Access the settings icon on the indicator to navigate the style and settings:

Length: Modifies the amount of data used to calculate the oscillator.

Signal: Further calibrates the sensitivity of the final plot.

High/Low Thresholds: A single filtration method for defining extreme zones of momentum bias, which determines entry/exits along with the zero line crosses.

Remaining Settings: Customize stop loss calibration along with optional features and styling choice.

Oscillators have been a staple in financial analysis since the mid-20th century, with tools like the RSI, MACD, and Stochastic helping gauge overbought and oversold conditions. What makes the latter unique is that the stochastic utilizes highs and lows as opposed to various EMA rates of change. Kinetik's unique boundless stochastic calculation and K/D difference plotting are the heart of this strategy.

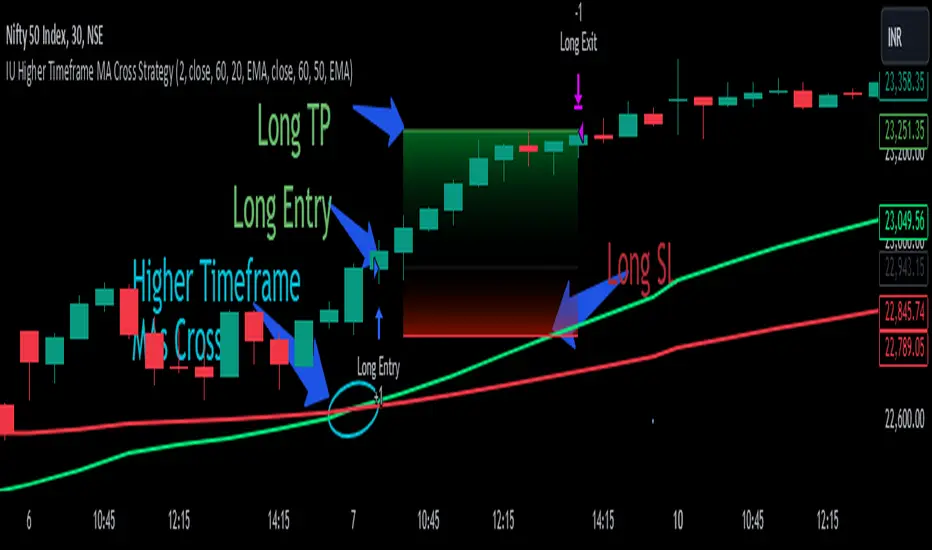

IU Higher Timeframe MA Cross StrategyIU Higher Timeframe MA Cross Strategy

The IU Higher Timeframe MA Cross Strategy is a versatile trading tool designed to identify trend by utilizing two customizable moving averages (MAs) across different timeframes and types. This strategy includes detailed entry and exit rules with fully configurable inputs, offering flexibility to suit various trading styles.

Key Features:

- Two moving averages (MA1 and MA2) with customizable types, lengths, sources, and timeframes.

- Both long and short trade setups based on MA crossovers.

- Integrated risk management with adjustable stop-loss and take-profit levels based on a user-defined risk-to-reward (RTR) ratio.

- Clear visualization of MAs, entry points, stop-loss, and take-profit zones.

Inputs:

1. Risk-to-Reward Ratio (RTR):

- Defines the take-profit level in relation to the stop-loss distance. Default is 2.

2. MA1 Settings:

- Source: Select the data source for calculating MA1 (e.g., close, open, high, low). Default is close.

- Timeframe: Specify the timeframe for MA1 calculation. Default is 60 (60-minute chart).

- Length: Set the lookback period for MA1 calculation. Default is 20.

- Type: Choose the type of moving average (options: SMA, EMA, SMMA, WMA, VWMA). Default is EMA.

- Smooth: Option to enable or disable smoothing of MA1 to merge gaps. Default is true.

3. MA2 Settings:

- Source: Select the data source for calculating MA2 (e.g., close, open, high, low). Default is close.

- Timeframe: Specify the timeframe for MA2 calculation. Default is 60 (60-minute chart).

- Length: Set the lookback period for MA2 calculation. Default is 50.

- Type: Choose the type of moving average (options: SMA, EMA, SMMA, WMA, VWMA). Default is EMA.

- Smooth: Option to enable or disable smoothing of MA2 to merge gaps. Default is true.

Entry Rules:

- Long Entry:

- Triggered when MA1 crosses above MA2 (crossover).

- Entry is confirmed only when the bar is closed and no existing position is active.

- Short Entry:

- Triggered when MA1 crosses below MA2 (crossunder).

- Entry is confirmed only when the bar is closed and no existing position is active.

Exit Rules:

- Stop-Loss:

- For long positions: Set at the low of the bar preceding the entry.

- For short positions: Set at the high of the bar preceding the entry.

- Take-Profit:

- For long positions: Calculated as (Entry Price - Stop-Loss) * RTR + Entry Price.

- For short positions: Calculated as Entry Price - (Stop-Loss - Entry Price) * RTR.

Visualization:

- Plots MA1 and MA2 on the chart with distinct colors for easy identification.

- Highlights stop-loss and take-profit levels using shaded zones for clear visual representation.

- Displays the entry level for active positions.

This strategy provides a robust framework for traders to identify and act on trend reversals while maintaining strict risk management. The flexibility of its inputs allows for seamless customization to adapt to various market conditions and trading preferences.

Pavan CPR Strategy Pavan CPR Strategy (Pine Script)

The Pavan CPR Strategy is a trading system based on the Central Pivot Range (CPR), designed to identify price breakouts and generate long trade signals. This strategy uses key CPR levels (Pivot, Top CPR, and Bottom CPR) calculated from the daily high, low, and close to inform trade decisions. Here's an overview of how the strategy works:

Key Components:

CPR Calculation:

The strategy calculates three critical CPR levels for each trading day:

Pivot (P): The central value, calculated as the average of the high, low, and close prices.

Top Central Pivot (TC): The midpoint of the daily high and low, acting as the resistance level.

Bottom Central Pivot (BC): Derived from the pivot and the top CPR, providing a support level.

The script uses request.security to fetch these CPR values from the daily timeframe, even when applied on intraday charts.

Trade Entry Condition:

A long position is initiated when:

The current price crosses above the Top CPR level (TC).

The previous close was below the Top CPR level, signaling a breakout above a key resistance level.

This condition aims to capture upward momentum as the price breaks above a significant level.

Exit Strategy:

Take Profit: The position is closed with a profit target set 50 points above the entry price.

Stop Loss: A stop loss is placed at the Pivot level to protect against unfavorable price movements.

Visual Reference:

The script plots the three CPR levels on the chart:

Pivot: Blue line.

Top CPR (TC): Green line.

Bottom CPR (BC): Red line.

These plotted levels provide visual guidance for identifying potential support and resistance zones.

Use Case:

The Pavan CPR Strategy is ideal for intraday traders who want to capitalize on price movements and breakouts above critical CPR levels. It provides clear entry and exit signals based on price action and is best used in conjunction with proper risk management.

Note: The strategy is written in Pine Script v5 for use on TradingView, and it is recommended to backtest and optimize it for the asset or market you are trading.

Stochastic RSI OHLC StrategyThe script titled "Stochastic RSI High Low Close Bars" is a versatile trading strategy implemented in Pine Script, designed for TradingView. Here's an overview of its features:

Description

This strategy leverages the Stochastic RSI to determine entry and exit signals in the market, focusing on high, low, and close values of the indicator. It incorporates various trading styles, stop-loss mechanisms, and multi-timeframe analysis to adapt to different market conditions.

Key Features

Stochastic RSI Analysis:

Uses the Stochastic RSI to identify potential entry points for long and short positions.

Tracks high, low, and close values for more granular analysis.

Multiple Trading Styles:

Supports diverse trading styles like Volume Color Swing, RSI Divergence, RSI Pullback, and more.

Allows switching between these styles to suit market dynamics.

Session-Based Trading:

Offers session control, limiting trades to specific hours (e.g., NY sessions).

Can close all positions at the end of the trading day.

Stop-Loss and Take-Profit Mechanisms:

Includes both static and dynamic stop-losses, with options for time-based stops, trailing stops, and momentum-based exits.

Customizable take-profit levels ensure efficient trade management.

Volume Analysis:

Integrates volume indicators to add a bias for trade entries and exits, enhancing signal reliability.

Multi-Timeframe Integration:

Employs multi-timeframe RSI analysis, allowing the strategy to capture broader trends and optimize entries.

This script is designed to provide flexibility and adaptability, making it useful for different trading strategies and market conditions. It is suitable for traders looking to refine their entries and exits with a focus on the Stochastic RSI.

Filtered Bollinger Bands By @TradingadeThis is a reversal strategy based on Bollinger Bands combined with a Trend filter.

The most important part of this strategy is the Trend filter. When applied, it will increase the likelihood of confirming an exhausted movement (it will help find the maximum "elastic bent"), and may reduce chances of getting bad entries condition.

The logic of this code is:

Enter Long : price goes outside lower band, then close cross above lower band

Stop Loss : Percentage %

Take profit : Percentage %

Exit Cond : when high crosses above upper band. It could be both in profit or in loss.

Filter: Yesterday low was the lowest in previous X days

Enter Short : price goes outside lower band, then close cross above lower band

Stop Loss : Percentage %

Take profit : Percentage %

Exit Cond : when low crosses below lower band. It could be both in profit or in loss.

Filter: Yesterday high was the highest in previous X days

FILTER Notes:

You could switch both timeframe and N. of candles in input section. Even tough generally daily data are more reliable, you could find interesting to change it to 1H tf, so filter would be:

"1H high/low was the lowest/highest in previous X hours"

EXIT Notes:

Please note that "% exits" will always override "Exit Cond".

Set % exits to 0 if you want to exit only by "Exit Cond".

Settings used to get the results below :

Initial Capital = 10000

Order Size = 10000 USDT

Commission = 0.06 %

TREND FILTER

Trend filter = True

Trend intensity = 4 Candles , TF 1 day

BB FILTER

Lenght = 20

Source = Close

StdDev = 2

STRATEGY SETTINGS

Position Side = LONG

Stop Loss % = 8

Take Profit % = 0

Exit Cond = True

Strategy Gaussian Anomaly DerivativeConcept behind this Strategy :

Considering a normal "buy/sell" situation, an asset would be bought in average at the median price following a Gaussian like concept. A higher or lower average trend would significate that the current perceived value is respectively higher or lower than the current median price, which mean that the buyers are evaluating the price underpriced or overpriced.

This behaviour would be even more relevent depending on its derivative evolution.

Therefore, this Strategy setup is based on this Gaussian like concept anomaly of average close positionning compare to high-low average derivative, such as the derivative of the following ploted basic signal : 1-(high+low)/(2*close).

This Strategy can actually be used like a trend change and continuation strength indicator aswell.

In the Setup Signal part :

You can define the filtering of the basis signal "1-(high+low)/(2*close)" on EMA or SMA as you wish.

You can define the corresponding period and the threathold as a mutiply of the average 1/3 of all time value of the basis signal.

You can define the SMA filtering period of the Derivative signal and the corresponding threathold on the same mutiply of the average 1/3 of all time value of the derivative.

In the Setup Strategy part :

You can set up your strategy assesment based on Long and/or Short. You can also define the considered period.

The most successful tuned strategies I did were based on the derivative indicator with periods on the basis signal and the derivative under 30, can be 1 to 3 of te derivative and 7 to 21 for the basis signal. The threathold depends on the asset volatility aswell, 1 is usually the most efficient but 0 to 10 can be relevent depending on the situation I met. You can find an example of tuning for this strategy based on Kering's case hereafter.

I hoping that you will enjoy using this Strategy, don't hesitate to comment, to question, to correct or complete it ! I would be very curious about similar famous approaches that would have already been made.

Thank to you !

Simple and Profitable Scalping Strategy (ForexSignals TV)Strategy is based on the "SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV.

See video for a detailed explaination of the whole strategy.

I'm not entirely happy with the performance of this strategy yet however I do believe it has potential as the concept makes a lot of sense.

I'm open to any ideas people have on how it could be improved.

Strategy incorporates the following features:

Risk management:

Configurable X% loss per stop (default to 1%)

Configurable R:R ratio

Trade entry:

Based on stratgey conditions outlined below

Trade exit:

Based on stratgey conditions outlined below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: On higher timeframe trend EMAs, Fast EMA must be above Slow EMA

C2: On higher timeframe trend EMAs, price must be above Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be above Medium EMA and Medium EMA must be above Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in upward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the high of the last X candles (plus price buffer) to trigger entry (stop order entry)

SHORT

C1: On higher timeframe trend EMAs, Fast EMA must be below Slow EMA

C2: On higher timeframe trend EMAs, price must be below Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be below Medium EMA and Medium EMA must be below Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in downward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the low of the last X candles (plus price buffer) to trigger entry (stop order entry)

Trade entry:

Calculated position size based on risk tolerance

Entry price is a stop order set just above (buffer configurable) the recent swing high/low (long/short)

Trade exit:

Stop Loss is set just below (buffer configurable) trigger candle's low/high (long/short)

Take Profit calculated from Stop Loss using R:R ratio

Credits

"SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV

MZ HTF HFT ROCit Bot - Non Repainting Scalper v1.2 ADX RSI MOM This is a new iteration based on my Momentum trading bot.

This is an original script meant to be a high frequency trader that works on higher time frame calculations.

I came up with the idea that using calculus I can figure out the actual rate of change and momentum with different calculations than the momentum indicator that is provided by trading view. Once momentum is shifted on a small time frame, it will provide an entry signal. The script is meant to be used on an algorithmic trading system for scalping purposes. It should be run on a one minute time frame. Unfortunately due to various plotting constraints in Pinescript, you cannot plot the rate of change and momentum and price in the same pane. To counter this, I have a showdata toggle to give you values of the indicators at each entry.

This version has two main entry settings toggled with a checkbox. There is the ROC (rate of change) version and the MOM (momentum) entry signals.

The rate of change version is meant to take a look at your moving average and try to trigger when it hits a certain rate of change point. This can be helpful if you rather play it safer. I have noticed that you can get slightly better entry points but also does not give you as many entries. The momentum algorithm will give you faster entry points and might work best with a slight offset (use your back test to help you figure it out).

I have started to add tooltips to help you along. If you have suggestions please let me know.

How does it work?

Let's just assume that you are looking at a one minute chart. I recommend using the one minute for bots because it will give you the fastest execution for entries. Pinescript has an issue where the signal is not usually sent until the end of the bar/beginning of next bar. If the signal was triggered at the beginning of a 15 minute bar, it might not actually send the signal until the following 15 minute bar. If you are trading on small time frames, this can make all the difference. If you are using an algo platform that trailing stops, stop losse, take profits, etc. I would recommend you use that platform to close your trade. The close trade message will work, but pinescript does not know the exact entry price you received, so if you are trying to collect small profits, it is best that intermediary platform does that calculation for you. If you are dealing with larger moves, instead of small 1-3% scalps, you are probably fine to use the close message setting from pinescript.

Ok, so to take an example. I like to use the 3L and 3S tokens on Kucoin. This gives you a lot of volatility to work with compared to other tokens and coins. However, it can also meas that you are likely taking a higher risk. However, there are some things that can help with that (more on that later).

So we have a token we want to run, and have it on the 1m chart.

First, be sure that all of your filters are OFF when you start playing with the back test. This allows you to see how to best optimize the bot.

Use the show data to show you additional data when you are backtesting. This can allow you to try to filter out results or market conditions that do not work. I typically work with the RSI and use the 30 minute and 15 minute RSIs. I make sure that it is trading within a certain band - about 40-75. You can try the inverse and only buy during really low RSI's as well.

www.dropbox.com

Find the source of your data with the variant drop down. You can use any time frame, open, close. high, low, olc4. Open is pretty much guaranteed to not have any repainting issues - although all the other calcs use a custom isbarconfirmed security repaint calculation. I have been finding that Open and SMA work well, but feel free to explore. If you use a source like open, close, high, low, etc - the interval will not change anything further. If you use a variant such as an sma, you should try to find an interval that works well for that token. For instance, try an sma of 8-11 minutes and see which gives you the best backtest result without changing anything else. Offset ALMA/LSMA parameters are only used for those specific variants. These specific parameters will also affect the ALMA and LSMA if you use that variant in the trend filter. In other words, you can skip these if you are not using those types of moving averages.

www.dropbox.com

Configure the ROC and MOM intervals. If you are using a source such as open, close, etc- this is where you set the interval for your change. So consider using OHLC4 or a interval of 5 thru 15 and see what works best. The Momentum inverval usually works best in the 2-5 bars. There is a custom calculation I added in to try to filter out false entries as momentum is waning. This calculation works best in 2-5 bar interval.

Configure the trigger point and offset. If you are using rate of change, the best settings will likely be between -1 to 0.5. If you are using momentum, you will likely want -20 to 10. This is where you will notice the entries will shift a bit. Try to find a balance between your backtest settings and actually finding what you thin will be the best entries based on a slight delay from trading view, to algo, to your trading platform. This can likely be a minute (maybe even) or so- so be sure to not get too caught up between the backtest results and be sure to finesse the entries to actually fit nicely - maybe a bar earlier than you would likely think. If your entries are coming in too early, you can use the offset to delay your entry by a few bars. This is both science and an art form- don't get too caught up on the back test results as that is based on having all the data tha already transpired, it's not based on how it will actually perform during deployment.

Take profit and stop loss. This should be self explanatory. This script can toggle between static take profit and a trailing profit. For scalping, you will likely want to limit it below 2% to get a good win ratio. Stop loss should be at least 5-6% for these types of 3L/3S tokens to give the strategy some room to move (if the token goes down 2% before it shoots back up, the price will go down 6%). This does not yield the best R/R ratio from a traditional trader perspective, but the statistical probabilities are in your favor for these events will happen. If you have better ideas for how to set this all up, feel free to contribute your ideas in the comments as we can all learn from each other. You can definitely set a much tighter stop loss with a larger take profit to get a lower win rate but in turn might get much better returns. It's all up to you.

FILTERS www.dropbox.com